Opinion: Redlining Revisited

By Tom Coale

The writer (@hocorising) is a land use and zoning attorney in Ellicott City. He sits on the board of directors for the Baltimore Regional Housing Partnership.

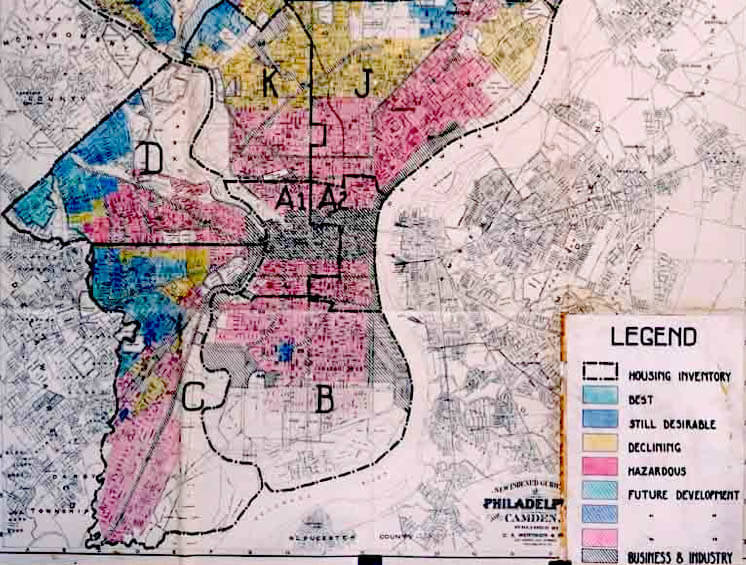

New research suggests that discriminatory lending practices that disadvantaged Black homeowners, popularized with the term “redlining,” preexisted and were much more widespread than the color-coded maps that gave rise to the term.

A new research paper written by Price V. Fishback, Jonathan Rose, Kenneth A. Snowden and Thomas Storrs and published by the National Bureau of Economic Research concluded that while the infamous maps created by the Home Owners’ Loan Corporation (HOLC) in the late 1930s were shared with the Federal Housing Administration, the latter agency had implemented its own discriminatory practices based on city-block level data independent of the HOLC maps. While we know the FHA created its own “redlined” map, such documents were destroyed in response to civil rights litigation in 1969.

As background, the HOLC was created in 1933 as a part of the New Deal to refinance home mortgages that were in default. The FHA was created a year later pursuant to the National Housing Act of 1934 for the purpose of increasing home-ownership by offering federally backed mortgage insurance.

Without such insurance, homeownership was limited to those who could put down 40% or more of a home purchase price at closing. Continuing to the present, the FHA made homeownership accessible to those who can afford as little as 5% down.

By extending homeownership to millions of Americans, FHA mortgage insurance has facilitated hundreds of billions of dollars in wealth creation for the White middle class.

Reviewing lending data for both entities, Fishback and his colleagues found that the share of loans refinanced by HOLC for Black Americans was close to proportionate to the share of homeowners who were Black.

In contrast, the FHA largely excluded low-income urban neighborhoods from its mortgage insurance program, which disproportionately excluded Black borrowers. Said otherwise, the single greatest government sponsored wealth transfer in this country’s history excluded Black borrowers while lifting up borrowers who were white.

While this truth has been woven into the understanding of “redline” lending practices, this new study demonstrates that FHA was much more engaged and deliberate in excluding Black families from the mortgage lending its insurance facilitated than previously realized.

Rather than the passive utilization of static maps, such as those produced by HOLC, FHA underwriters would diligently research the racial dynamics of neighborhoods down to the street level when deciding whether to insure a mortgage.

Ultimately, this study acquits HOLC as the driver of inequitable lending practices and places it more in the position of reflecting existing conditions created by the FHA.

Fishback and colleagues note that the FHA was created to encourage “economically sound” loans mostly utilized in the suburbs, while the HOLC was a temporary relief program to assist homeowners in refinancing distressed mortgages. This distinction continues when contrasting government programs intended to foster economic growth to poverty prevention and intervention measures. The former are most often available and utilized by White citizens while the latter are promoted paternalistically toward people of color.

Citizens and lawmakers should utilize this new information to reflect on lending and housing policy with a larger scope that is not constrained to city maps with red, blue and yellow neighborhoods. During its formative years, FHA was facilitating White flight and the growth of the suburbs with particularized racist intent and application. Racial covenants preventing the sale of homes had long since been declared illegal, but our financial institutions provided a vanguard against full integration.

Racially discriminatory lending practices are what make socioeconomic segregation look like racial segregation.

We cannot go back and offer non-discriminatory loans to people of color in 1935. And it is upon this basis that thought leaders like Ta-Nehisi Coates have endorsed reparations premised on the distribution of wealth to White families during the first half of the 20th century. Maryland has within its means the ability to direct financial resources to Black prospective homeowners who have been deprived of generational wealth created by entities like the FHA.

Housing discussions need not be constrained to the binary of subsidized and market rate. White Americans have utilized residential structures as nest eggs for generations and did so at the enticement of the federal government. It is time Black Americans have an equal opportunity to participate as well.

Maryland Matters welcomes guest commentary submissions at [email protected]. We suggest a 750-word limit and reserve the right to edit or reject submissions. We do not accept columns that are endorsements of candidates or submissions from political candidates. Views of writers are their own.

Related Articles

An earlier commentary glossed over the facts at the heart of the dispute over this Historic East Towson housing project.

This ideal affordable housing project – and others like it – are desperately needed

Maryland is in the midst of a housing crisis. According to statistics compiled by Maryland Realtors, the average sale price of a home in…

Creative Commons Attribution

Creative Commons Attribution