One of the most persistent myths plaguing our discussion of the housing crisis is that market rate housing “does nothing” for affordable housing or, even more problematic, makes it worse.

During a recent forum on affordable housing, Montgomery County Executive Marc Elrich stated that because there was no “affordable housing requirement” for accessory dwelling units (also known as ADUs), these units did not support affordable housing. He went on to say that “no one in the field” believed that increasing the supply of market rate housing would serve the goals of providing affordable housing.

In both instances, County Executive Elrich was wrong.

As with any other market, housing prices are driven by high-income purchasers. In a jurisdiction that allows for housing development, those purchasers will customarily be attracted to new market rate units, which carry the highest cost per square foot. When new market rate units are not available, the high-income purchaser will turn to the existing housing stock and, in doing so, push housing prices higher throughout the entire spectrum of housing options.

This high-income purchaser will out-bid middle-income purchasers who will then turn to the next available level of housing. The middle-income purchaser outbids those with lower incomes who do not qualify for subsidized housing. The ultimate result is that the housing available for middle-income families is hollowed out, housing is bought up by high-income purchasers, and a marginal amount of housing is set aside for low-income families, creating housing distribution across income levels resembling a lopsided barbell.

The results of this are seen in Maryland jurisdictions, such as Montgomery County, that have adopted housing moratoria over the last half decade and now see housing prices escalate at rates as high as 10% year over year. Such housing moratoria have been created on the premise that public infrastructure, such as roads and schools, needs time to “catch up” to population growth, yet there is no evidence that population growth is stopped, or even slowed, by caps on development.

Rather, as sales prices and property valuations balloon pursuant to the scenario described above, empty nesters are incentivized to sell their homes to new families, which increases the turnover of existing housing stock. Infrastructure burdens continue to mount, which prompt renewed calls from housing opponents to stop new development and increase regulations, taxes and fees on the non-existent new development being blamed for these ills.

The cycle continues, prices escalate and barriers rise for low- and middle-income families seeking access to high-opportunity areas.

One of the worst consequences of this cycle is the effect on housing vouchers, which allow low-income renters to find housing in high-opportunity areas by funding the difference between market rents and what the family is able to pay. When housing prices escalate, so do rents. As rents become more expensive, housing vouchers lose their purchasing power and providers are forced to spend more their limited resources keeping up with the widening gap.

In this way, housing moratoria and limits on new development affirmatively work against affordable housing and make large swaths of Maryland inaccessible to low-income families.

New market rate housing does not create affordable housing, but it does slow the escalation of housing prices and increase the overall affordability of housing in the jurisdiction.

Local and state housing policy must begin with the premise that housing growth should continue at a reasonable pace set by the general plan while additional avenues are pursued to provide housing for low-income families, such as public housing, housing vouchers and density incentives for affordable set-aside units. Innovative housing policies, such as the legalization of ADUs in single-family detached zones, also utilize the market to provide additional access points for middle-income residents to find housing in high-opportunity areas.

In the announcement of his $2 trillion infrastructure package, President Biden identified the primary barriers to affordable housing as “minimum lot sizes, mandatory parking requirements and prohibitions on multifamily housing,” the staples of suburban zoning regulations. He has further allocated $5 billion of this package to a grant program, which will award funds to jurisdictions that “take concrete steps to eliminate such needless barriers to producing affordable housing.”

Housing advocates are encouraging federal lawmakers to take this one step further and penalize states with local jurisdictions that leave these barriers in place. A recent poll conducted by Data for Progress shows that the majority of voters support making infrastructure spending contingent on local governments adopting pro-housing policies that encourage the development of multifamily housing.

Maryland jurisdictions need to get out of the mindset that affordable housing objectives can be met without market rate development or that the two are somehow separate.

We need a holistic approach to housing that includes increasing supply, protecting renters and government-owned housing. Any one without the other is doomed to fail.

— TOM COALE

The writer is a land use and zoning attorney with the law firm of Talkin & Oh LLP in Ellicott City. He represents affordable housing developers throughout the state.

Maryland Matters welcomes guest commentary submissions at [email protected]. We suggest a 750-word limit and reserve the right to edit or reject submissions. We do not accept columns that are endorsements of candidates or submissions from political candidates. Views of writers are their own.

Related Articles

House Bill 538, aiming to incentivize developers to add affordable housing options in future developments, lagged behind Moore’s other two housing-centered bills.

This ideal affordable housing project – and others like it – are desperately needed

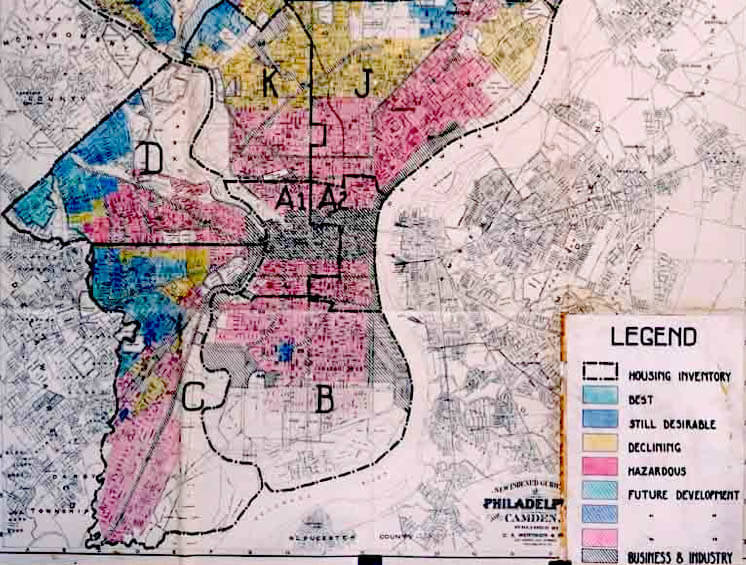

New research suggests that discriminatory lending practices that disadvantaged Black homeowners, popularized with the term “redlining,” preexisted and were much more widespread than the color-coded maps that gave rise to the term.

Creative Commons Attribution

Creative Commons Attribution